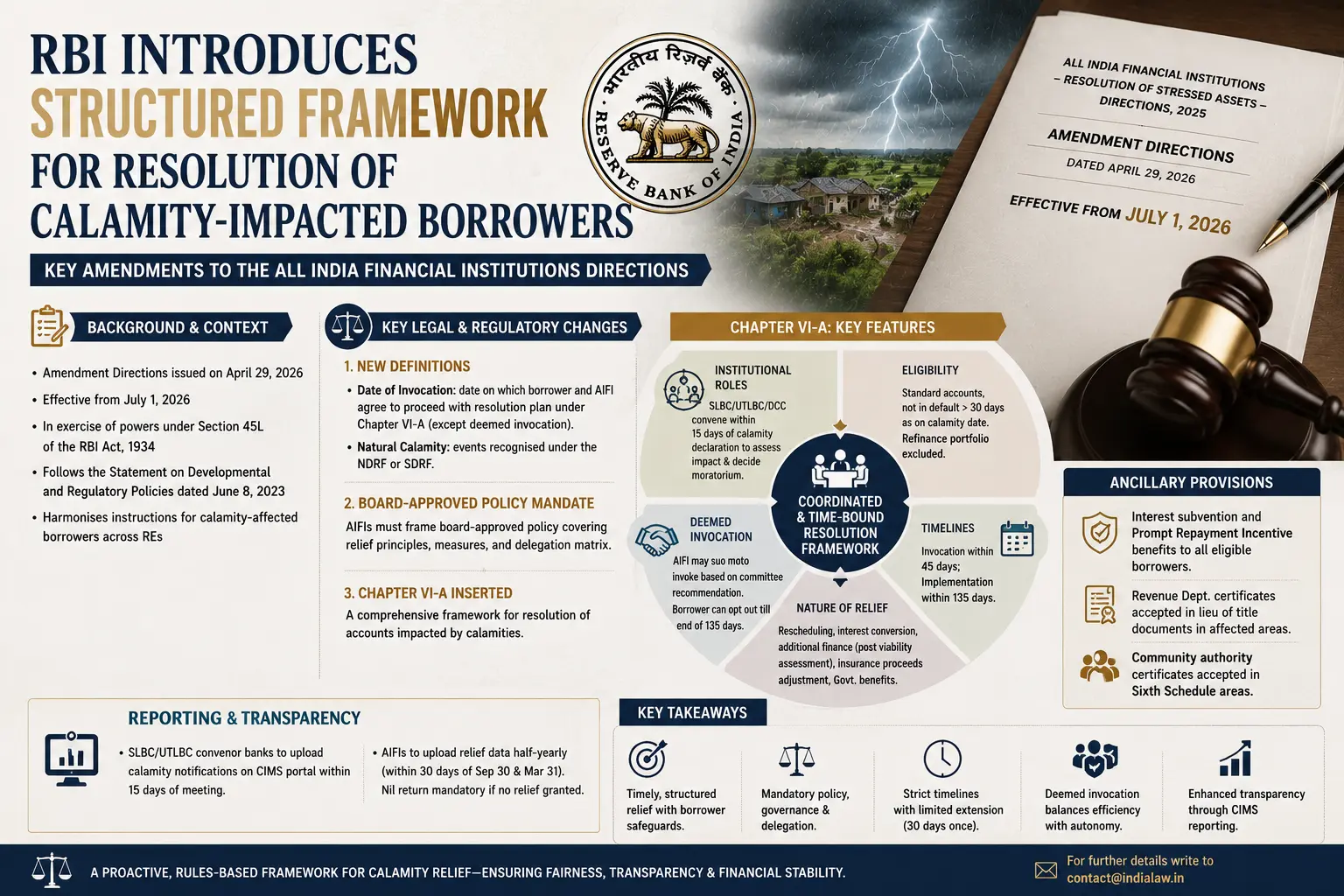

RBI Introduces Structured Framework for Resolution of Calamity-Impacted Borrowers: Key Amendments to the All India Financial Institutions Directions

The Reserve Bank of India has introduced a dedicated regulatory framework for resolving loan accounts of borrowers affected by natural calamities and certain external disruptions. These Amendment Directions, effective July 1, 2026, modify the RBI’s Principal Directions on resolution of stressed assets for All India Financial Institutions.

Background and Context

The Reserve Bank of India (RBI) has, by way of its Amendment Directions dated April 29, 2026, introduced a dedicated regulatory framework for the resolution of loan accounts of borrowers adversely affected by natural calamities and certain other external disruptions. These amendments modify the Reserve Bank of India (All India Financial Institutions – Resolution of Stressed Assets) Directions, 2025 (the “Principal Directions”), and will come into force with effect from July 1, 2026.

The regulatory impetus for this intervention dates to the Statement on Developmental and Regulatory Policies issued by the Reserve Bank on June 8, 2023, in which the RBI signalled its intention to rationalise prudential norms governing the implementation of resolution plans for exposures affected by natural calamities. The stated objective was to harmonise instructions applicable across different categories of Regulated Entities (REs).

Following a comprehensive review of existing regulatory instructions — encompassing scope, coverage, and prudential requirements — draft Directions were circulated for public comment before being finalised in their present form.

The Amendment Directions have been issued in exercise of the powers vested in the Reserve Bank under Section 45L of the Reserve Bank of India Act, 1934.

Key Legal and Regulatory Changes

New Definitions

Two important definitional insertions have been made to Paragraph 4 of the Principal Directions.

“Date of invocation” (Paragraph 4(3A)) is defined as the date on which the borrower and the All India Financial Institution (AIFI) agree, through a documented arrangement, to proceed with a resolution plan under the newly inserted Chapter VI-A, except in cases of deemed invocation as provided under Paragraph 119N.

“Natural calamity” (Paragraph 4(8A)) is defined with reference to events recognised under the National Disaster Response Fund (NDRF) or the State Disaster Response Fund (SDRF). This statutory anchoring is significant: it ties eligibility for the calamity-resolution framework to a pre-existing governmental classification mechanism, thereby reducing the scope for discretionary or inconsistent interpretation at the institutional level.

Board-Approved Policy Mandate

A new Paragraph 12A requires every AIFI to incorporate provisions for calamity-related resolution into its board-approved policy. At minimum, the policy must address:

- Objective principles governing the terms of relief to be granted across borrower and loan categories.

- The potential relief measures available, together with verifiable parameters for determining their applicability.

- A delegation matrix for deciding and implementing relief measures, including restructuring and sanction of additional finance, with a specific emphasis on timely execution.

This requirement places the governance of calamity-linked resolution squarely within institutional risk management architecture. It signals a move away from ad hoc relief dispensation towards a rules-based, auditable framework operating under board oversight.

Chapter VI-A: Resolution of Accounts Impacted by Calamities

The centrepiece of the Amendment Directions is the insertion of Chapter VI-A, which contains a comprehensive set of instructions governing the identification, invocation, implementation, and reporting of resolution plans for calamity-affected borrowers.

The chapter operates upon the declaration of a calamity — whether natural or arising from external events such as riots or civil disturbances — by the Central or State Government, in accordance with the relevant governmental framework.

Importantly, accounts in which relief measures have already been extended as of the effective date of the Amendment Directions are not disturbed; they will continue to be governed by the existing prudential guidelines. However, any fresh resolution in such accounts after July 1, 2026, must comply with Chapter VI-A.

Institutional Roles and Procedural Architecture

State Level Bankers’ Committee / District Consultative Committee

Chapter VI-A assigns a structured coordinating role to the State Level Bankers’ Committee (SLBC), Union Territory Level Bankers’ Committee (UTLBC), and District Consultative Committee (DCC). Upon the declaration of a calamity:

- Where a larger part of a State or UT has been affected, the SLBC/UTLBC convenor bank must convene a special meeting within 15 days of declaration.

- Where only a part of the State or UT is affected, the DCC convenor for the affected district(s) convenes the meeting within the same period.

These meetings are intended to assess the severity of the calamity’s economic impact, identify impacted borrowers using objective criteria, and determine the extent of any moratorium period.

Decisions taken at these meetings are to be circulated promptly to all SLBC/UTLBC/DCC members, relevant Regional Offices of the Reserve Bank, and NBFCs and Urban Co-operative Banks operating in the affected area.

Adequate publicity through brochures, newspapers, field visits, and other suitable modes is also mandated — a practical acknowledgment that relief frameworks are of limited value if borrowers are unaware of them.

Eligibility, Invocation, and Implementation

Eligibility

Only borrowers whose accounts are classified as “Standard” and are not in default by more than 30 days with the AIFI in respect of any facility, as on the date of occurrence of the calamity, are eligible for resolution under Chapter VI-A.

Where no specific date of occurrence is ascertainable, the date of the governmental declaration of the calamity serves as the operative date. Borrowers who do not satisfy these conditions may still be considered for resolution under other provisions of the Principal Directions.

The chapter explicitly excludes the refinance portfolio of an AIFI from its scope.

Timelines

Resolution must be invoked no later than 45 days from the date of declaration of the calamity and must be implemented within 135 days from the same date. These are hard timelines, subject to one exception.

Where neither deemed invocation is feasible nor can the AIFI complete invocation formalities within the 45-day window, the SLBC/UTLBC/DCC convenor may apply to the relevant Regional Director or Officer-in-Charge of the Reserve Bank for a one-time extension of 30 days. Any such request must detail the reasons for the delay and is assessed on its individual merits.

Deemed Invocation

One of the more notable features of Chapter VI-A is the provision for suo moto or “deemed” invocation (Paragraph 119N). An AIFI is not required to wait for a formal request from the borrower; it may unilaterally implement a resolution plan consequent to the SLBC/UTLBC/DCC’s recommendations. In such cases, the resolution is deemed invoked from the date of the committee’s decision.

However, a critical safeguard accompanies this power: the AIFI must communicate the deemed invocation to the borrower and must preserve the borrower’s right to opt out of the resolution plan at any point until the end of the 135-day implementation window. This opt-out right reflects a measured balance between institutional efficiency and borrower autonomy.

Nature of Resolution Plans

Resolution plans may encompass a range of measures tailored to the borrower’s circumstances:

- Rescheduling of payments.

- Conversion of accrued or accruing interest into another credit facility.

- Sanction of additional finance to address financial stress, subject to viability assessment.

The framework thus permits a graduated and context-sensitive response, rather than prescribing a single template for all affected accounts.

Ancillary and Protective Measures

Chapter VI-A includes several borrower-protective provisions of practical significance. AIFIs are required to account for any insurance proceeds receivable in respect of restructured accounts, though they may extend restructuring and sanction fresh loans without waiting for actual receipt of such claims.

Interest subvention and Prompt Repayment Incentive (PRI) benefits, as notified by the Government from time to time, must be extended to all eligible borrowers without exception.

For agricultural loans secured against land, the directions recognise documentary challenges in calamity-affected areas. Revenue Department certificates are to be accepted as a substitute for original title records where a borrower has lost proof of title.

In areas governed by the Sixth Schedule of the Constitution where land is owned communally, certificates issued by community authorities are similarly acceptable.

Reporting and Transparency

The framework introduces a structured reporting regime through the Centralised Information Management System (CIMS) portal. SLBC/UTLBC convenor banks are required to upload governmental calamity notifications within 15 days of the relevant special meeting.

AIFIs must upload data on relief measures on a half-yearly basis, within 30 days of the close of each half-year (September 30 and March 31). Where no relief measures have been extended, a nil return is required.

This reporting discipline enables the Reserve Bank to monitor the real-time effectiveness of the framework and identify systemic gaps in implementation.

Concluding Observations

The Reserve Bank of India’s Amendment Directions represent a substantive and long-overdue effort to institutionalise the resolution of calamity-linked credit stress within the formal regulatory framework applicable to All India Financial Institutions.

By introducing time-bound invocation and implementation windows, a board-level policy mandate, and borrower-protective safeguards including the opt-out right and nil-return obligations, the RBI has signalled a clear preference for structured, auditable, and borrower-sensitive relief delivery over discretionary case-by-case responses.

The deemed invocation mechanism, in particular, is a pragmatic innovation: it enables institutional action in environments where borrower outreach may be physically or logistically impractical in the immediate aftermath of a calamity. Combined with the opt-out safeguard, it addresses both efficiency and autonomy concerns simultaneously.

Institutions should treat the July 1, 2026 effective date as a firm deadline and initiate policy revision, delegation restructuring, and system preparation immediately. The broader signal from this amendment is unmistakable: the RBI expects its regulated entities to be proactive, not merely reactive, in discharging their obligations to borrowers in distress.

This article is intended for general informational purposes only and does not constitute legal advice. Readers should seek specific legal counsel in relation to the matters discussed herein.

By entering the email address you agree to our Privacy Policy.